SBFN Member Since:

2013

Member Organisations

Bangko Sentral ng Pilipinas (Central Bank of the Philippines)

Department of Environmental and Natural Resources of the Philippines (DENR)

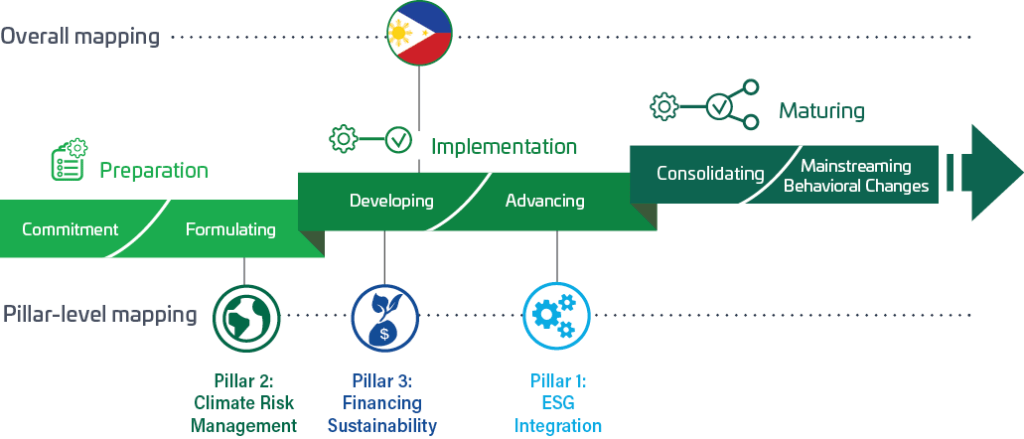

Progress Against sub Pillars

Framework Documents

| Country | Policies/ Principles/ Guidelines | Year | Issuer |

|---|---|---|---|

| Philippines | Circular 1128 Series of 2021 – Environmental and Social Risk Management Framework | 2021 | Bangko Sentral ng Pilipinas (BSP, Central Bank of Philippines) |

| Philippines | 2021 | Philippines Inter-Agency Technical Working Group for Sustainable Finance (ITSF) | |

| Philippines | 2020 | Bangko Sentral ng Pilipinas (BSP, Central Bank of Philippines) | |

| Philippines | 2020 | Philippines Securities and Exchange Commission | |

| Philippines | Sustainability Reporting Guidelines for Publicly Listed Companies | 2019 | Philippines Securities and Exchange Commission |

Pillar 1 - ESG Integration - Strategic Alignment

National Framework

P 1.1 – Has the regulator or industry association published a national framework (“Framework”) for the banking sector that sets out expectations for integrating the consideration of environmental, social, and governance (ESG) risks and performance?

Yes

Source Reference Detail

The Philippines Securities and Exchange Commission announced in 2019 the requirement of sustainability reporting on a comply or explain basis for all listed companies, together with the publication of a guidance. The guidance is intended to help listed companies assess and manage non-financial performance across economic, environmental and social aspects of their organization and enable listed companies to measure and monitor their contributions towards achieving universal targets of sustainability, such as the UN’s Sustainable Development Goals as well as national policies and programs, such as AmBisyon Natin 2040.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

–

P 1.2 – Has the relevant regulator or industry association published a Framework for capital markets, investment, insurance or other non-lending FIs that sets out expectations for integrating the consideration of environmental, social, and governance (ESG) risks and performance?

Yes

Source Reference Detail

The SEC, aside from the Sustainability Reporting Guidelines, has also issued in 2018 and 2019 the Guidelines pertaining to the issuance of Green, Social, and Sustainability Bonds.The Philippines Securities and Exchange Commission announced in 2019 the requirement of sustainability reporting on a comply or explain basis for all listed companies, together with the publication of a guidance. The guidance is intended to help listed companies assess and manage non-financial performance across economic, environmental and social aspects of their organization and enable listed companies to measure and monitor their contributions towards achieving universal targets of sustainability, such as the UN’s Sustainable Development Goals as well as national policies and programs, such as AmBisyon Natin 2040.

Source Reference Document

Guidelines on Issuance of Sustainability Bonds 2020

Source Reference Description

–

Pillar 1 - ESG Integration - Strategic Alignment

Alignment with International Goals & Standards

P 1.3 – Does the Framework make reference to international sustainable development frameworks or goals?

Yes

Source Reference Detail

The Sustainability Reporting Framework by the SEC makes reference to: SDGs, Global Reporting Initiative (GRI), Sustainability Reporting Standards, International Integrated Reporting Council (IIRC), Integrated Reporting (IR) Framework, Sustainability Accounting Standards Board (SASB), Sustainability Accounting Standards, TCFD.Also, the BSP’s Sustainable Finance Framework made reference to the aspirations set out in the Philippine Development Plan which incorporates the SDGs.

Source Reference Document

Sustainability Reporting Guidelines for Publicly Listed CompaniesSustainable Finance Framework 2020

Source Reference Description

–

P 1.4 – Does the Framework make reference to established international ESG risk management standards and principles for FIs??

Yes

Source Reference Detail

The Philippines Securities and Exchange Commission announced in 2019 the requirement of sustainability reporting on a comply or explain basis for all listed companies, together with the publication of a guidance. The guidance is intended to help listed companies assess and manage non-financial performance across economic, environmental and social aspects of their organization and enable listed companies to measure and monitor their contributions towards achieving universal targets of sustainability, such as the UN’s Sustainable Development Goals as well as national policies and programs, such as AmBisyon Natin 2040.

Source Reference Document

Sustainability Reporting Guidelines for Publicly Listed Companies

Source Reference Description

–

Pillar 1 - ESG Integration - Strategic Alignment

Alignment with national goals & strategies

P 1.5 – Does the Framework make reference to specific national development objectives, plans, policies, goals, or targets?

Yes

Source Reference Detail

The Bangko Sentral likewise recognizes the critical role of the financial industry in pursuing sustainable and resilient growth by enabling environmentally and socially responsible business decisions consistent iwth the aspirations set out for the Fillipinos under the philippine Development Plan.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 1, Policy Statement

P 1.6 – Does any cooperation exist between agencies or between the regulator and industry association with respect to policy design and/or implementation related to ESG integration?

Yes

Source Reference Detail

There is an inter-agency working group on sustainable finance, dubbed as the “Green Force”.

Source Reference Document

Sustainable Finance Working Group “Green Force”

Source Reference Description

–

P 1.7 – Does any inter-agency data sharing currently exist related to ESG integration by FIs?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

Pillar 1 - ESG Integration - Regulatory and Industry Association Actions

Overall Approach & Strategy

P 1.8 – Does the Framework provide guidance on the role of the regulator or industry association with regard to assessing and managing ESG risk and performance in the financial sector?

Yes

Source Reference Detail

The Bangko Sentral expects banks to embed sustainability principles, including those covering environmental and social risk areas, in their corporate governance framework, risk management systems, and strategic objectives consistent with their size, risk profile and complexity of operations.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 1, Policy Statement

P 1.9 – Has the regulator or industry association undertaken market assessment to identify systemic ESG risks through analysis of the portfolios of supervised entities/members and published the results?

Yes

Source Reference Detail

The BSP conducted a study entitled “Impact of Extreme Weather Episodes on the Philippine Banking Sector: Evidence Using Branch-Level Supervisory Data”. The study argues that natural disasters and severe weather-related events pose risks that can potentially and unintentionally affect the stability of the banking system. This study confirms the effects of severe weather conditions on the banking sector performance.Moreover, the BSP has yet to conduct a vulnerability assessment and climate stress testing exercises with pilot banks.

Source Reference Document

Central Bank of the Philippines study “Impact of Extreme Weather Episodes on the Philippine Banking Sector: Evidence Using Branch-Level Supervisory Data”(2020)

Source Reference Description

–

Pillar 1 - ESG Integration - Regulatory and Industry Association Actions

Technical Guidance

P 1.10 – Does the Framework provide technical guidance or tools to support implementation of ESG risk and performance management by the financial sector?

Yes

Source Reference Detail

–

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 3, ESRMS Guidance

Pillar 1 - ESG Integration - Regulatory and Industry Association Actions

Supervisory Activities & incentives

P 1.11 – Is the implementation of the Framework regularly monitored and/or information regularly collected from FIs by the regulator and/or industry association?

Yes

Source Reference Detail

Banks shall also disclose in their annual report the progress of implementation of initiatives undertaken to integrate sustainability principles in their governance framework, risk management system, business strategy and operations.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 4, Disclosoure Requirements

P 1.12 – Does the regulator or industry association provide any financial or non-financial incentives for FIs to manage ESG performance as part of the Framework?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

P 1.13 – Does the regulator or industry association apply any disincentives/penalties for non-compliance by FIs in terms of expectations from the regulator and/or industry association related to ESG risk management as part of the Framework?

Yes

Source Reference Detail

After the lapse of the transition period provided in the Sustainable Finance Framework, any non-compliance of banks with the provisions of the Framework are automatically subjected to the overall Supervisory Enforcement Policy of the BSP as provided under Section 002 of the MORB.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

–

Pillar 1 - ESG Integration - Regulatory and Industry Association Actions

Tracking & Aggregated Disclosure

P 1.14 – Has the regulator or industry association established a data collection approach and database to track or regularly publish data related to ESG integration by FIs as part of the Framework?

Yes

Source Reference Detail

Approve the bank’s ESRMS that is commensurate with the bank’s size, nature, and complexity of operations and oversee its implementation.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 4, Disclosoure Requirements

Pillar 1 - ESG Integration - Expectations of FI Actions

Strategy & Governance

P 1.15 – Does the Framework require/ask the FI’s board of directors (or highest governing body) to approve an ESRM and/or ESG integration strategy, and to supervise its implementation?

Yes

Source Reference Detail

Approve the bank’s ESRMS that is commensurate with the bank’s size, nature, and complexity of operations and oversee its implementation.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 2 Board of Directors para c

Pillar 1 - ESG Integration - Expectations of FI Actions

Organizational Structure & Capacity Building

P 1.16 – Does the Framework require/ask FIs to allocate resources/budget commensurate with portfolio ESG risks and define roles and responsibilities for ESG integration within the organization?

Yes

Source Reference Detail

Ensure that adequate resources are available to attaint the bank’s sustainability objectives.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 3, Board of Directors

P 1.17 – Does the Framework require/ask FIs to develop and maintain the ESG expertise and capacity of staff commensurate with portfolio ESG risks through regular training and learning?

Yes

Source Reference Detail

Identify the unit or personnel responsible for overseeing the management of E&S risks.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 4, ESRMS

P 1.18 – Does the Framework require/ask FIs to create incentives for managers to reduce the ESG risk-level of the portfolio over a specified timeframe?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

Pillar 1 - ESG Integration - Expectations of FI Actions

Policies & Procedures

P 1.19 – Does the Framework require/ask FIs to develop policies and procedures to identify, classify, measure, monitor, and manage ESG risks and performance throughout the financing cycle at the client level and/or the transaction/project level?

Yes

Source Reference Detail

b, Provide clear guidance in assessing E&S risks in the bank’s oeprations, products and services, transactions, activities, and operating environment.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 3, ESRMS

P 1.20 – Does the Framework require/ask FIs to undertake a regular review and monitoring of ESG risk exposure at aggregate portfolio level?

Yes

Source Reference Detail

a. Define the level of risk appetite of the bank on E&S risk. The scope and complexity of the ESRMS shall be commensurate with the level of E&S risks associated with the bank’s portfolio.cc. Provide the tools for monitoring E&S risks as well as the compliance of the bank

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 3, ESRMS

P 1.21 – Does the Framework require/ask FIs to establish and maintain an external inquiry/complaints/grievance mechanism for interested and affected stakeholders in relation to ESG practices?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

Pillar 1 - ESG Integration - Expectations of FI Actions

Tracking, Reporting & Disclosure

P 1.22 – Does the Framework require/ask FIs to report ESG risks and performance to the regulator or industry association?

Yes

Source Reference Detail

The ESG risks and performance are among the items to be disclosed by banks in their Annual Reports to be submitted to the BSP.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

–

P 1.23 – Does the Framework require/ask FIs to report on ESG integration publicly?

Yes

Source Reference Detail

Banks shall disclosure the following information in their Annual Reports: Overview of E&S risk management system, Breakdown of E&S risk exposures of the bank per industry or sector, Information on existing and emerging E&S risks and their impact on the bank. The Sustainable Finance Framework also provides that if the required disclosures are captured in the Sustainability Report that is being submitted by publicly listed banks to the SEC, the Sustainability Report may be submitted together with the Annual Report to the BSP.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 4, Disclosoure Requirements

P 1.24 – Does the Framework require/ask FIs to track credit risk (e.g. loan defaults) and/or financial returns in relation to ESG risk level?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

Pillar 2 - Climate Risk Management - Strategic Alignment

National Framework

P 2.25 – Has the regulator or industry association published a national framework (“Framework”) for the banking sector that sets out expectations for integrating the consideration and management of climate risks and their impact in the national economy?

Yes

Source Reference Detail

Central Bank of the Philippines, Cicular 1085 (2020) Sustainable Finance Framework. Definition of terms, parts b, c, d, and e reference climate-related risks and physical and transition risks as part of E&S issues for ESG risk management. Philippines Securities and Exchange Commission (SEC) Memorandum Circular (MC) No. 4 Sustainability Reporting Guidelines for Publicly-Listed Companies and Guide which includes reporting requirements for PLCs using international guidelines including the Taskforce for Climate-related Financial Disclosures (TCFD) (2019).

Source Reference Document

Sustainability Reporting Guidelines for Publicly Listed CompaniesSustainable Finance Framework

Source Reference Description

Definition of terms parts b – d

P 2.26 – Has the relevant regulator or industry association published a Framework for capital markets, investment, insurance or other non-lending FIs that sets out expectations for integrating the consideration and management of climate risks and their impact in the national economy?

Yes

Source Reference Detail

Philippines Securities and Exchange Commission (SEC) Memorandum Circular (MC) No. 4 Sustainability Reporting Guidelines for Publicly-Listed Companies and Guide which includes reporting requirements for PLCs using international guidelines including the Taskforce for Climate-related Financial Disclosures (TCFD) (2019).

Source Reference Document

Sustainability Reporting Guidelines for Publicly Listed Companies

Source Reference Description

Philippines Securities and Exchange Commission (SEC) Memorandum Circular (MC) No. 4 Sustainability Reporting Guidelines for Publicly-Listed Companies and Guide which includes reporting requirements for PLCs using international guidelines including the Taskforce for Climate-related Financial Disclosures (TCFD) (2019).

Pillar 2 - Climate Risk Management - Strategic Alignment

Alignment with International Goals & Standards

P 2.27 – Does the Framework make reference to international agreements or frameworks to address climate?

Yes

Source Reference Detail

Central Bank of the Philippines, Cicular 1085 (2020) Sustainable Finance Framework refers in the Policy Statement (Page 1) to the Philippines Development Plan. The 2019 Philipines Voluntary National Review on SDG progress (including SDG 13 on climate change) includes the Philippines Development Plan (Section 2: Main Messages of the Philippines VNR, page 4 of 50).

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Central Bank of the Philippines, Cicular 1085 (2020) Sustainable Finance Framework refers in the Policy Statement (Page 1) to the Philippines Development Plan. The 2019 Philipines Voluntary National Review on SDG progress (including SDG 13 on climate change) includes the Philippines Development Plan (Section 2: Main Messages of the Philippines VNR, page 4 of 50).

P 2.28 – Does the Framework recognize or align with established regional or international good practice for climate risk management and disclosure by FIs?

Yes

Source Reference Detail

Central Bank of the Philippines, Cicular 1085 (2020) Sustainable Finance Framework, Disclosure Requirements (Page 4) refers to the Sustainability Reporting for Publicly Listed Entities. Philippines Securities and Exchange Commission (SEC) Memorandum Circular (MC) No. 4 Sustainability Reporting Guidelines for Publicly-Listed Companies and Guide which includes reporting requirements for PLCs using international guidelines including the Taskforce for Climate-related Financial Disclosures (TCFD) (2019)

Source Reference Document

Sustainable Finance Framework 2020Sustainability Reporting Guidelines for Publicly Listed Companies

Source Reference Description

(1) Page 4

Pillar 2 - Climate Risk Management - Strategic Alignment

Alignment with National Goals & Strategies

P 2.29 – Has the regulator or industry association aligned the Framework with national goals to address climate change in line with the country’s Nationally Determined Contributions (NDCs) to the Paris Agreement?

Yes

Source Reference Detail

Central Bank of the Philippines, Cicular 1085 (2020) Sustainable Finance Framework refers in the Policy Statement (Page 1) to the Philippines Development Plan. The 2019 Philipines Voluntary National Review on SDG progress (including SDG 13 on climate change) references the Paris Agreement and the Philippines Nationally Determined Contibution (NDC), Page 31.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 1, Policy Statement

P 2.30 – Does any cooperation exist between agencies, or between government and industry association, with respect to policy design or implementation related to climate risk management?

Yes

Source Reference Detail

Central Bank of the Philippines undertakes regulatory-industry collaboration on sustainable finance and climate risk, including with the Minsitries of Finance and Energy, respectively, as part fo the sustainable finance working group (“Green Force”).

Source Reference Document

Sustainable Finance Working Group “Green Force”

Source Reference Description

–

P 2.31 – Does any inter-agency data sharing currently exist related to climate risk management by FIs?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

Pillar 2 - Climate Risk Management - Regulatory and Industry Association Actions

Overall Approach & Strategy

P 2.32 – Has the regulator or industry association undertaken research on historical impacts to the economy and financial sector from climate change, and/or future expected impacts resulting from physical and transition climate risks?

Yes

Source Reference Detail

Central Bank of the Philippines conducted study: “Impact of Extreme Weather Episodes on the Philippine Banking Sector: Evidence Using Branch-Level Supervisory Data”. (2020)

Source Reference Document

Central Bank of the Philippines study “Impact of Extreme Weather Episodes on the Philippine Banking Sector: Evidence Using Branch-Level Supervisory Data”(2020)

Source Reference Description

–

P 2.33 -Does the Framework identify key sources of GHG emissions – such as in particular sectors – as priorities in the proactive management of climate risks by the financial sector?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

P 2.34 – Does the Framework incorporate the conservation/restoration of natural carbon sinks (such as oceans, forests, mangroves, grasslands, and soils) as an important part of reducing climate change risks? (e.g., through guidelines, scenario analysis, targets, or incentives for FIs)

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

P 2.35 – Has the regulator or industry association developed an internal strategy to address climate risk, and/or embedded climate risk management into its governance, organizational structures, and budget as part of the Framework?

Yes

Source Reference Detail

Central Bank of the Philippines, Cicular 1085 (2020) Sustainable Finance Framework refers in the Introduction the embedding of ESG and climate risk in its approach to the banking sector: “The Monetary Board, in its Resolution 415, dated 19 March 2020, approved the sustainable finance policy framework that sets out the expectations fo the Central Bank on the integration of sustainability principles, including those covering ESG risks areas, in the corporate governance and risk management frameworks, as well as in the strategic objectives and operations of the banks. Per Section 153 of the Manual on the Regulations of Banks.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Introduction

P 2.36 – Has the regulator or industry association undertaken any activities to expand and deepen analytical understanding of national and/or cross-border physical and transition climate risks, and to raise awareness as to how these risks may transmit to, and impact, the financial sector?

Yes

Source Reference Detail

Central Bank of the Philippines undertakes regulatory-industry collaboration on sustainable finance and climate risk, including with the Minsitries of Finance and Energy, respectively, as part of the sustainable finance working group (“Green Force”).

Source Reference Document

Sustainable Finance Working Group “Green Force”

Source Reference Description

–

Pillar 2 - Climate Risk Management - Regulatory and Industry Association Actions

Technical Guidance

P 2.37 – Has the regulator or industry association developed risk assessment approaches, methodologies, or tools to understand and assess the financial sector’s exposure to climate risk as part of the Framework?

Yes

Source Reference Detail

Central Bank of the Philippines conducted study: “Impact of Extreme Weather Episodes on the Philippine Banking Sector: Evidence Using Branch-Level Supervisory Data”. (2020). This study will form the basis for the future developemnt of regulatory guidance.

Source Reference Document

Central Bank of the Philippines study “Impact of Extreme Weather Episodes on the Philippine Banking Sector: Evidence Using Branch-Level Supervisory Data”(2020)

Source Reference Description

–

Pillar 2 - Climate Risk Management - Regulatory and Industry Association Actions

Supervisory Activities & Incentives

P 2.38 – As part of the Framework, has the regulator clarified supervisory expectations with regard to climate risk management by FIs, including consideration of international good practices?

No

Source Reference Detail

Central Bank of the Philippines, Cicular 1085 (2020) Sustainable Finance Framework refers in the Introduction the embedding of ESG and climate risk in its approach to the banking sector: “The Monetary Board, in its Resolution 415, dated 19 March 2020, approved the sustainable finance policy framework that sets out the expectations fo the Central Bank on the integration of sustainability principles, including those covering ESG risks areas, in the corporate governance and risk management frameworks, as well as in the strategic objectives and operations of the banks. Per Section 153 of the Manual on the Regulations of Banks.”

Source Reference Document

Sustainable Finance Framework

Source Reference Description

–

P 2.39 – Has the regulator started to explicitly embed climate-related risk in supervisory activities and review processes as part of the Framework?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

P 2.40 – Has the regulator started to explicitly embed climate-related risk in supervisory activities and review processes as part of the Framework?

Yes

Source Reference Detail

Central Bank of the Philippines, Cicular 1085 (2020) Sustainable Finance Framework, Disclosure Requirements (Page 4) points a) through f) as part of the Annual Report. The requirements also reference the Sustainability Reporting for Publicly Listed Entities as part of the Philippines Securities and Exchange Commission (SEC) Memorandum Circular (MC) No. 4 Sustainability Reporting Guidelines for Publicly-Listed Companies and Guide which includes reporting requirements for PLCs using international guidelines including the Taskforce for Climate-related Financial Disclosures (TCFD) (2019)

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 4

P 2.41 – Has the regulator started to explicitly embed climate-related risk in supervisory activities and review processes as part of the Framework?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

Page 4

Pillar 2 - Climate Risk Management - Regulatory and Industry Association Actions

Tracking & Aggregated Disclosure

P 2.42 – Does the regulator or industry association regularly collect and/or report market-level and/or FI-level data on climate-related financial sector risks as part of the Framework?

Yes

Source Reference Detail

Central Bank of the Philippines, Cicular 1085 (2020) Sustainable Finance Framework, Disclosure Requirements (Page 4) points a) through f) as part of the Annual Report. The requiremetns also reference the Sustainability Reporting for Publicly Listed Entities as part of the Philippines Securities and Exchange Commission (SEC) Memorandum Circular (MC) No. 4 Sustainability Reporting Guidelines for Publicly-Listed Companies and Guide which includes reporting requirements for PLCs using international guidelines including the Taskforce for Climate-related Financial Disclosures (TCFD) (2019).

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Pillar 2 - Climate Risk Management - Expectations of FI Actions

Strategy & Governance

P 2.43 – Does the Framework require/ask FIs to establish a strategy for climate risk management with responsibility at the board of director level (or highest governing body)?

Yes

Source Reference Detail

Central Bank of the Philippines, Cicular 1085 (2020) Sustainable Finance Framework, Section Duties and Responsibilities of the Board and Senior Management, Point A calls for the incorporation of ESG and climate risk in the bank’s strategic objectives, corporate governance and risk management.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Point a

Pillar 2 - Climate Risk Management - Expectations of FI Actions

Organizational Structure & Capacity Building

P 2.44 – Does the Framework require/ask FIs to define the roles and responsibilities and related capacities of the FI’s senior management and operational staff in identifying, assessing, and managing climate-related financial risks and opportunities?

Yes

Source Reference Detail

Central Bank of the Philippines, Cicular 1085 (2020) Sustainable Finance Framework, Section Duties and Responsibilities of the Board and Senior Management. Section Board of Directors, Points a) through g); and Senior Management points a) through d) collectively address governance of ESG and lcimate risks and organizational responsibilities and capacity.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Points a – g

Pillar 2 - Climate Risk Management - Expectations of FI Actions

Policies & Procedures

P 2.45 – Does the Framework require/ask FIs to expand existing risk management processes to identify, measure, monitor, and manage/mitigate financial risks from climate change?

Yes

Source Reference Detail

Central Bank of the Philippines, Cicular 1085 (2020) Sustainable Finance Framework, Section Definition of Terms, Points b), c), d), and e) reference climate-related risks and physical and transition risks as part of E&S issues for ESG risk management. Section Environmental and Social Risk Management System (ESRMS) Points a) through f) define risk identification, exposure assessment, stress testing, and use of scenarios (short and long term time horizons), and management of these risks.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Points b – e

Pillar 2 - Climate Risk Management - Regulatory and Industry Association Actions

Tracking, reporting & disclosure

P 2.46 – Does the Framework require/ask FIs to report on their overall approaches to climate risk management in line with international good practices (e.g., TCFD), or establish a timeline by which FIs should begin to align their reporting with such practices?

Yes

Source Reference Detail

Central Bank of the Philippines, Cicular 1085 (2020) Sustainable Finance Framework, Disclosure Requirements (Page 4) points a) through f) as part of the Annual Report. The requirements also reference the Sustainability Reporting for Publicly Listed Entities as part of the Philippines Securities and Exchange Commission (SEC) Memorandum Circular (MC) No. 4 Sustainability Reporting Guidelines for Publicly-Listed Companies and Guide which includes reporting requirements for PLCs using international guidelines including the Taskforce for Climate-related Financial Disclosures (TCFD) (2019).

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Central Bank of the Philippines, Cicular 1085 (2020) Sustainable Finance Framework, Disclosure Requirements (Page 4) points a) through f) as part of the Annual Report. The requirements also reference the Sustainability Reporting for Publicly Listed Entities as part of the Philippines Securities and Exchange Commission (SEC) Memorandum Circular (MC) No. 4 Sustainability Reporting Guidelines for Publicly-Listed Companies and Guide which includes reporting requirements for PLCs using international guidelines including the Taskforce for Climate-related Financial Disclosures (TCFD) (2019).

P 2.47 – Does the Framework require/ask FIs to identify, measure, and report on exposure to sectors which are vulnerable to transition risk and physical risk?

Yes

Source Reference Detail

Central Bank of the Philippines, Cicular 1085 (2020) Sustainable Finance Framework, Section Definition of Terms, Points b), c), d), and e) reference climate-related risks and physical and transition risks as part of E&S issues for ESG risk management. Section Environmental and Social Risk Management System (ESRMS) Points a) through f) define risk identification, exposure assessment, stress testing, and use of scenarios (short and long term time horizons), and management of these risks.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Points b – e

P 2.48 – Does the Framework require/ask FIs to adopt and report on performance targets to reduce portfolio greenhouse gas (GHG) emissions on a regular basis?

Yes

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

P 2.49 – Does the Framework require/ask FIs to adopt and report on performance targets to reduce exposure to climate change risks at the portfolio level on a regular basis?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

Pillar 3 - Financing Sustainability - Strategic Alignment

National Framework

P 3.50 – Has the regulator or industry association published a national framework (“Framework”) for the banking sector that sets out expectations for integrating the consideration of instruments, goals, and standards for financing sustainability, including requirements for ensuring credibility and managing and measuring resulting impacts in the national economy?

Yes

Source Reference Detail

BSP’s SF Framework, page 2, para 1 “This also covers green finance which is designed to facilitate the flow of funds towards green economic activities and climate change mitigatin and adaptation projects. “

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 2, para 1

P 3.51 – Has the relevant regulator or industry association published a Framework for capital markets, investment, insurance or other non-lending FIs that sets out expectations for integrating the consideration of instruments, goals, and standards for financing sustainability, including requirements for ensuring credibility and managing and measuring resulting impacts in the national economy

Yes

Source Reference Detail

The SEC, aside from the Sustainability Reporting Guidelines, had also issued in 2018 and 2019 the Guidelines pertaining to the issuance of Green, SOcial, and Sustainability Bonds.

Source Reference Document

Sustainability Reporting Guidelines for Publicly Listed CompaniesGuidelines on Issuance of Sustainability Bonds

Source Reference Description

–

Pillar 3 - Financing Sustainability - Strategic Alignment

Alignment with International Goals & Standards

P 3.52 – Has the regulator or industry association developed a strategy, regulations, or set of frameworks for stimulating the allocation of capital to sustainable assets, projects, and related sectors in line with global goals, such as the Sustainable Development Goals (SDGs)?

Yes

Source Reference Detail

The Philippines Securities and Exchange Commission Sustainability Reporting Guidelines for Publicly-Listed Companies mentioned SDGs, page 14.The BSP’s Sustainable Finance Framework expects that banks’ ESrMS shall define the level of risk appetite on E&S risk. Hence, thresholds on allocating to sustainable assets or projects will vary across banks depending on their internal assessment and capacity to bear and manage such risk.

Source Reference Document

Sustainability Reporting Guidelines for Publicly Listed CompaniesSustainable Finance Framework 2020

Source Reference Description

–

P 3.53 – Does the Framework recognize and/or align with existing standards, voluntary principles, or market good practices related to sustainable finance instruments?

Yes

Source Reference Detail

The SEC, aside from the Sustainability Reporting Guidelines, had also issued in 2018 and 2019 the Guidelines pertaining to the issuance of Green, SOcial, and Sustainability Bonds.The SEC guidelines are patterned after ASEAN Standards and ICMA Principles.

Source Reference Document

Sustainability Reporting Guidelines for Publicly Listed CompaniesGuidelines on Issuance of Sustainability Bonds

Source Reference Description

Page 1, ICMA

Pillar 3 - Financing Sustainability - Regulatory and Industry Association Actions

Alignment with national goals & strategies

P 3.54 – Does the Framework enable the achievement of stated national objectives by guiding capital to sectors, assets, and projects that have environmental and social benefits in line with national sustainable development priorities, strategies, targets, and the size of sustainable investment needs, and taking into account the local barriers to scaling-up sustainable finance?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

P 3.55 – Does the Framework enable the achievement of stated national objectives by guiding capital to sectors, assets, and projects that have environmental and social benefits in line with national sustainable development priorities, strategies, targets, and the size of sustainable investment needs, and taking into account the local barriers to scaling-up sustainable finance?

Yes

Source Reference Detail

There is an inter-agency working group on sustainable finance, dubbed as the “Green Force”.

Source Reference Document

Sustainable Finance Working Group “Green Force”

Source Reference Description

–

P 3.56 – Does any inter-agency data sharing currently exist related to stimulating and monitoring sustainable finance flows?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

Pillar 3 - Financing Sustainability - Strategic Alignment

Overall Approach & Strategy

P 3.57 – Does the Framework require/ask the regulator or industry association to establish mechanisms to identify and encourage the allocation of capital to sustainable sectors, assets, and projects?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

Pillar 3 - Financing Sustainability - Regulatory and Industry Association Actions

Technical Guidance

P 3.58 – Does the Framework require/ask the regulator or industry association to establish mechanisms to identify and encourage the allocation of capital to sustainable sectors, assets, and projects?

Yes

Source Reference Detail

The SEC, aside from the Sustainability Reporting Guidelines, had also issued in 2018 and 2019 the Guidelines pertaining to the issuance of Green, SOcial, and Sustainability Bonds. The SEC guidelines are patterned after ASEAN Standards and ICMA Principles. The Guidelines provide the classification or categories of eligible projects. The Green Force is developing the principles-based taxonomy.

Source Reference Document

Sustainability Reporting Guidelines for Publicly Listed CompaniesGuidelines on Issuance of Sustainability BondsSustainable Finance Working Group “Green Force”

Source Reference Description

–

P 3.59 – Does the Framework provide guidelines for extending green, social or sustainability-focused loans (excluding bonds)?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

P 3.60 – Does the Framework provide guidelines for issuance of green, social or sustainability bonds?

Yes

Source Reference Detail

The Guidelines on Issuance of Green/Sustainability Bonds under the ASEAN Green/Sustainability Bond Standards issued by the Securities Exchange Commssion promote financing sustainability in the capital markets.The SEC, aside from the Sustainability Reporting Guidelines, had also issued in 2018 and 2019 the Guidelines pertaining to the issuance of Green, SOcial, and Sustainability Bonds.The SEC guidelines are patterned after ASEAN Standards and ICMA Principles. The Guidelines provide the classification or categories of eligible projects.

Source Reference Document

Sustainability Reporting Guidelines for Publicly Listed CompaniesGuidelines on Issuance of Sustainability BondsSustainable Finance Working Group “Green Force”

Source Reference Description

–

P 3.61 – Does the Framework require/ask for external party verification to ensure the credibility of sustainability instruments?

Yes

Source Reference Detail

Philippines recognize the ASEAN Green Bond Standards, which has such requirements.The SEC, aside from the Sustainability Reporting Guidelines, had also issued in 2018 and 2019 the Guidelines pertaining to the issuance of Green, SOcial, and Sustainability Bonds.The SEC guidelines are patterned after ASEAN Standards and ICMA Principles. The Guidelines provide the classification or categories of eligible projects.

Source Reference Document

Sustainability Reporting Guidelines for Publicly Listed CompaniesGuidelines on Issuance of Sustainability BondsSustainable Finance Working Group “Green Force”

Source Reference Description

–

Pillar 3 - Financing Sustainability - Regulatory and Industry Association Actions -

Supervisory activities & incentives

P 3.62 – Does the regulator or industry association monitor information reported by FIs related to green/social/sustainability investment, lending, and other instruments to prevent greenwashing and social-washing?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

P 3.63 – Are there any financial or non-financial incentives for FIs to develop and grow green, social, or sustainability finance instruments?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

Pillar 3 - Financing Sustainability - Regulatory and Industry Association Actions -

Tracking & Aggregated Disclosure

P 3.64 – Does the regulator or industry association collect and/or publish data from FIs or other sources about allocation of capital to green/social/sustainability assets, projects, or sectors?

Yes

Source Reference Detail

The SEC published on a monthly basis the Sustainable Finance Market Update about the green, social and sustainability bond issuances of Philippine companies.

Source Reference Document

Sustainable Finance Market Update

Source Reference Description

–

Pillar 3 - Financing Sustainability - Expectations of FI Actions

Strategy & Governance

P 3.65 – Does the Framework require/ask FIs to establish a strategy, governance, or high-level targets, including at the Board of Directors level, for capital allocation to sustainable assets, projects, or sectors?

Yes

Source Reference Detail

The BSP’s Sustainable Finance Framework expects that banks’ ESRMS shall define the level of risk appetite on E&S risk. Hence, thresholds on allocating to sustainable assets or projects will vary across banks depending on their internal assessment and capacity to bear and manage such risk.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 2, Board of Directors, Item d

Pillar 3 - Financing Sustainability - Expectations of FI Actions

Organizational Structure & Capacity Building

P 3.66 – Does the Framework require/ask FIs to define internal staff roles and responsibilities to encourage finance flows to green, social, and/or sustainability-focused investments?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

P 3.67 – Does the Framework require/ask FIs to develop and maintain internal staff capacity on green, social, or sustainability products through regular training and learning?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

Pillar 3 - Financing Sustainability - Expectations of FI Actions

Policies & Procedures

P 3.68 – Does the Framework require/ask FIs to put in place policies and procedures for defining, issuing, managing proceeds, tracking performance, and reporting on green, social or sustainability-focused products?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

P 3.69 – Does the Framework require/ask FIs to appoint an independent external reviewer to confirm that the FI’s internal framework meets the requirements of the recognized national framework and regulations, or aligns to international standards?

Yes

Source Reference Detail

The SEC, aside from the Sustainability Reporting Guidelines, had also issued in 2018 and 2019 the Guidelines pertaining to the issuance of Green, SOcial, and Sustainability Bonds.The SEC guidelines are patterned after ASEAN Standards and ICMA Principles. The Guidelines provide the classification or categories of eligible projects.

Source Reference Document

Sustainability Reporting Guidelines for Publicly Listed CompaniesGuidelines on Issuance of Sustainability Bonds

Source Reference Description

–

P 3.70 – Does the Framework require/ask that FIs create incentives for managers to increase sustainable loans or investments in the portfolio?

No

Source Reference Detail

Source Reference Document

–

Source Reference Description

–

Pillar 3 - Financing Sustainability - Expectations of FI Actions

Tracking, reporting & disclosure

P 3.71 – Does the Framework require/ask FIs to publish annual updates on the performance and impacts of the sustainability instruments in compliance with relevant national and/or international standards?

Yes

Source Reference Detail

Sustainable Finance Framework 2020, page 4, Disclosure Requirements, c. Products/services aligned with internationally recognized sustainability standards and practices. This shall include the issuance of green, social and sustainability bonds.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 4

P 3.72 – Does the Framework require/ask FIs to obtain and disclose independent review of metrics reported annually in relation to the social and environmental outcomes and impacts achieved through the sustainability instruments?

Yes

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

P 3.73 – Does the Framework require/ask FIs to obtain and disclose independent review of metrics reported annually in relation to the social and environmental outcomes and impacts achieved through the sustainability instruments?

No

Source Reference Detail

–

Source Reference Document

–

Source Reference Description

–

P 3.74 – Does the Framework require/ask FIs to report to the regulator(s) or industry association(s) on green, social, and/or sustainability bonds or other positive impact investments?

Yes

Source Reference Detail

c. Products/services aligned with internationally recognized sustainability standards and practices. This shall include the issuance of green, social and sustainability bonds.

Source Reference Document

Sustainable Finance Framework 2020

Source Reference Description

Page 4, Disclosure requirements, c.

P 3.75 – Does the Framework require/ask FIs to report publicly on their green, social and sustainability-focused finance activities and positive outcomes or impacts (i.e. not only to the regulator or shareholders)?

Yes

Source Reference Detail

–

Source Reference Document

Guidelines on Issuance of Sustainability Bonds 2020

Source Reference Description

Section C